India has the Second Highest Global Fintech Adoption Rate

- Posted on Oct 15, 2018

- |

- By Leena Bhagchandani

A significant evolving demographic of the Fintech sector, is the remarkably high receptiveness of Fintech solutions in the Indian sub-continent. India ranks second with 52% adoption rate only behind China at 69%; as per the EY Fintech Adoption Index 2017.

The cash-driven Indian economy has responded well to the fintech industry, prominently triggered by the rise in e-commerce, and increasing penetration of smartphones.

YES BANK, India’s fourth largest private-sector bank along with Pricewaterhouse Coopers (PwC), Let’s Talk Payments (LTP), Ourcrowd (global crowdfunding leader) and Burnmark (Research Partner); undertook the INDIA FINTECH OPPORTUNITIES REVIEW (IFOR). The report puts forward favorable factors that collectively will make India, a fintech hub. The country has the potential to emerge into the world-class fintech ecosystem and the opportunities are explored in the research.

About Fintech:

Fintech refers to the technological changes in the design and delivery of the financial services to the consumers. It uses Artificial Intelligence, Big Data, Machine Learning and other such advanced concepts to deliver greater consumer experience. It bridges the gap between traditional banking services and expected levels of user experience.

Fintech includes alternative payment methods, like the mobile wallets which propagate the use of digital money. Crypto currency is also an alternative to be used as a global digital money. Another widely used fintech platforms, include Comparison sites for purchasing insurance and banking products. Crowd funding, peer-to-peer lending sites, robo-advisory platforms and personal financial management (PFM) sites; have emerged as advanced solutions for financing and asset management.

India’s Fintech Landscape:

According to a KPMG – Google report, Fintech would drive 5X more employment, increase MSME contribution to the GDP by 10 percentage points, by 2022.

That being said, the question than arises: What can be done to make fintech businesses in India, sustainable? The findings from IFOR state, Fintech in India is still an inchoate sector. “Wherein,

- 64% of these organizations have been in business for 3 years or less

- Median employee strength is 14

- Dominated by young tech entrepreneurs

- 25% – less than 30 years of age

- 35% – between the age of 31-40

- 34% have less than 2 years of experience, 60% have less than 5 years of experience

- 91% have a STEM background

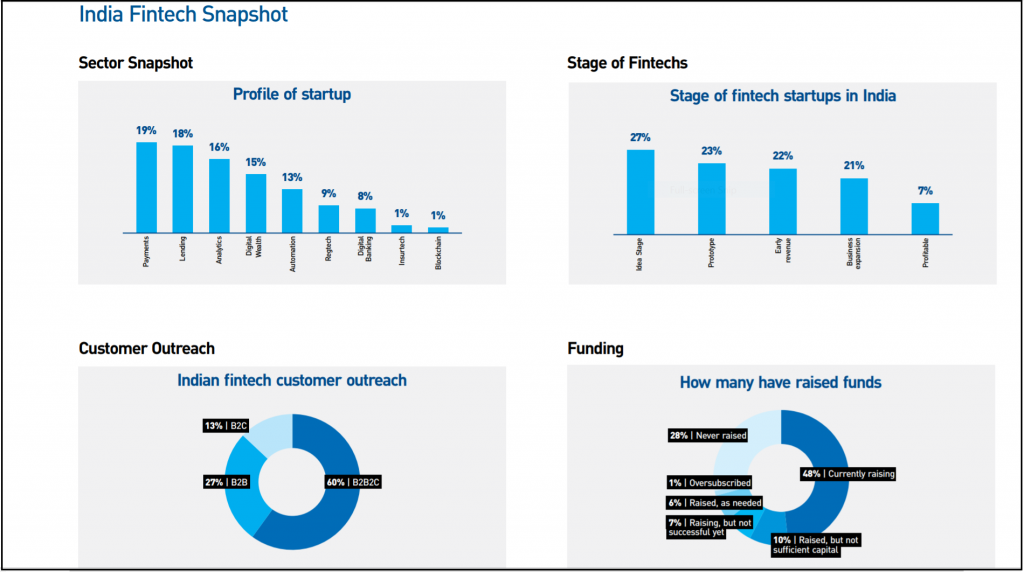

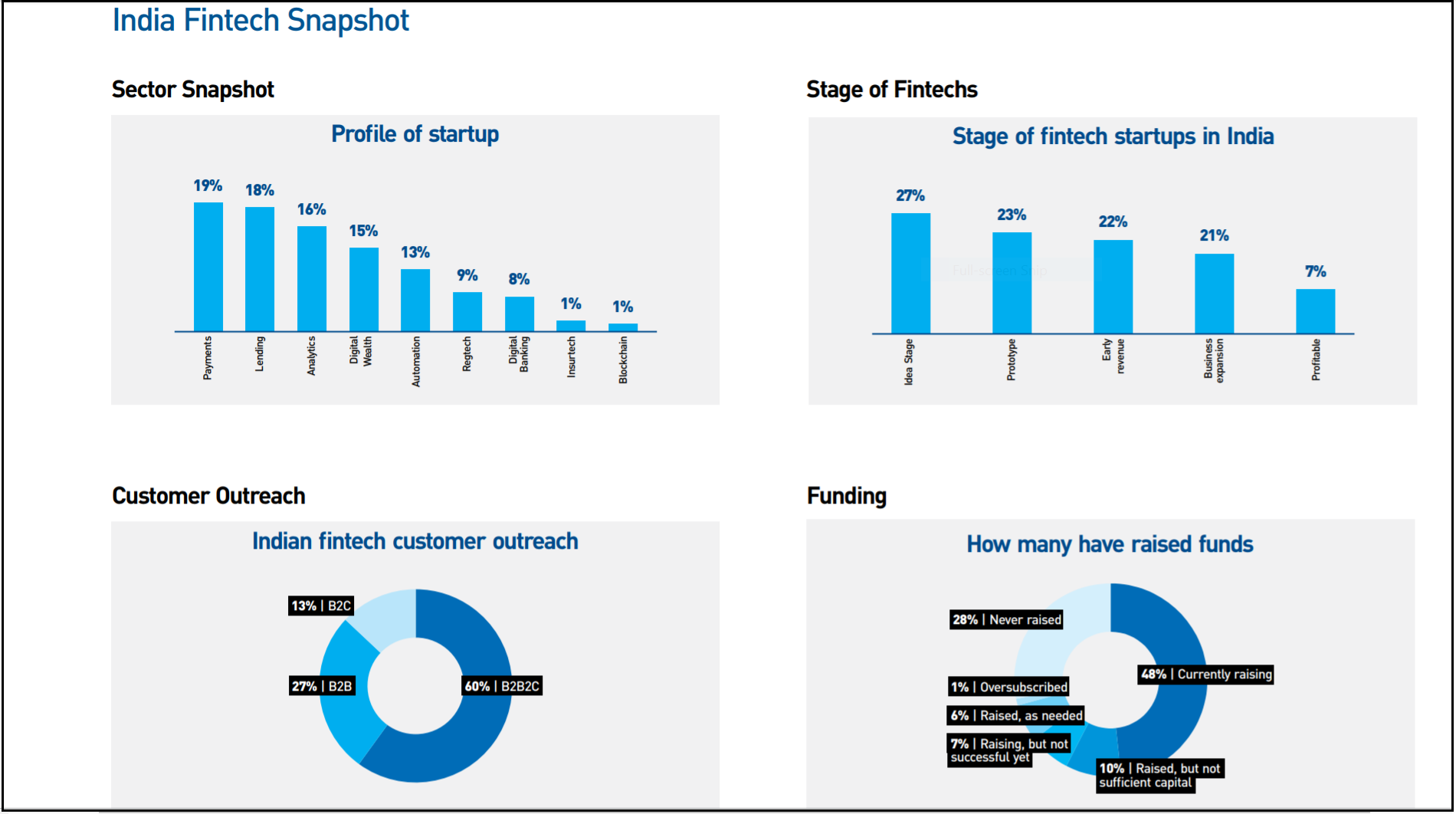

Fintechs in India are spread evenly (21%-27%) across ideation, prototype, early revenue and business expansion stages. Given the vintage of most of these startups; it is quite commendable that 7% of fintechs have already turned profitable.

While many equate Fintech in India as largely digital payments, the sector has evolved considerably with domains like digital wealth management, lending and robotics process automation picking up rapidly.”

Source:India Fintech Opportunities Review Report 2017-18

Major Fintech Hubs in the world:

-

London

London is an attractive location for fintech ecosystem as the city has the largest financial services sector and a booming technology sector. The city has: An ingenious financial workforce, Regulatory and Government support, Solid Funding Landscape and High Digital connectivity. It has undertaken the following major steps:

- UK’s Financial Conduct Authority(FCA) has its regulatory Sandbox for the companies to test their products under temporary regulations. It has included a mandate in its governance to support innovation and competition along with consumer protection and financial stability.

- FCA has also set up an advisory board that mentors fintech entrepreneurs on the regulations to be kept in mind while launching new products in the market. The initiative is under Project Innovate which fosters small businesses into developing better products.

London has so far provided the best regulatory support to fintech in terms of taxation and risk management, to name a few.

-

Singapore

Singapore, the leading International Finance Center, the highest smartphones penetration. i.e 80% and one of the highest levels of per capita income; makes it favorable city for developing the fintech ecosystem. The government has taken various initiatives to develop a favorable environment;

- Monetary Authority of Singapore (MAS) has appointed a Chief Fintech Officer and a Chief Data Officer. They would be responsible for enhancing the regulatory framework in the city to better foster innovation and management of risks in the fintech sector.

- International banks and global consultants have set up innovation labs in the financial sector to drive research and development.

Young talent, headquarter for 5 global banks, growing investments in the city along-with favorable policy environment; make Singapore the fintech hub.

-

Hong Kong

Hong Kong is Asia’s largest financial center and its proximity to China has lead to recent developments for fintech Industry. Government and Venture Capitalists have shown tremendous faith and their investments have contributed in turning Hong Kong into a fintech hub. Major efforts in the direction are as follows:

- Universities have played a major role by emphasizing the fintech industry. They have put in efforts for developing talent and leadership in the traditional workforce.

- Hong Kong’s Applied Science and Technology Research Institute has partnered with private, public and academic sector to develop fintech solutions.

With government support and promising talent, Hong Kong is on the path way of growth and development of fintech industry.

-

Australia

Australia raises as much as 14% of the total global funding raised; it has emerged as strong consumption ground for financial sector. The government has set up an advisory council to advise the Treasury in developing AUSTRALIA the leading market for fintech innovation. Key initiatives include the following:

- Australian Securities and Investments Commission (ASIC)’s creation of a regulatory sandbox for Fintechs

- Active support of Fintech solutions, from government include:

- promotion of greater data availability, including standard APIs to support Fintech innovators

- tax concessions for investments in Fintech

- a national cyber-security center

- overseas ‘landing pads’ for Australian Fintechs to operate overseas

- a regulatory framework to support equity and debt-based crowdfunding.

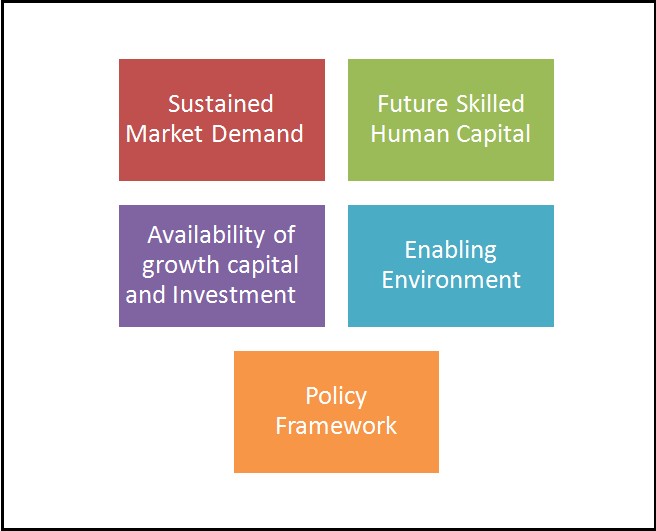

After studying major fintech hubs of the world; the report proposes 5 key factors that majorly contribute in developing ‘A Fintech Hub’

Key Enablers Of a Fintech Ecosystem:

The report lists down the findings for each of these enablers. The highlights are listed below:

-

Sustained Market Demand

- Unified Payment Interface (UPI) – transaction volume has grown from 0.1 million in Oct 16 to 79 million in Oct 17.

- Rs 26.5 trillion of SME debt demand unmet by formal channels.

- 72% of Fintech respondents across sectors found investment comparatively ‘easy’ post acquisition of their first enterprise customer (for B2B Fintechs).

- During IFOR research, it found out that 90% of startups fail in early stage either due to lack of data to test the innovative solutions or a corporate partner or funding.

-

Future Skilled Human Capital

- 33% of total employee strength comprises of coders, this number is as high as 67% in idea and pre-revenue stage startups.

- Current available talent pool is rich in technology graduates,but low on future tech skills or knowledge.

- Skilled Tech Talent retention presents a challenge for non-funded, bootstrapped Fintechs

-

Availability of growth and capital Investment

- 71% of pre-revenue and 81% idea stage Fintechs noted ‘severe difficulty’ in raising funds.

- Founder’s Educational background and experience appear to influence funding.

- Only 11% of respondents focusing on the B2B segment described fund raise as ‘easy’ or ‘moderately easy’.

- 74% of the startups have a burn rate between $10k-50k per annum and only 7% of them are profitable.

- Government Funds are available but respondents and industry experts indicate that the process and criteria are ambiguous.

-

Enabling Environment

- There is a need to bring the academia and industry closer to Fintechs, facilitating idea and information exchange

- A representative Fintech body can enhance the support network for assistance in mentoring, commercialization and development of Proofs of Concepts (PoCs).

- 71% of early/PoC stage respondents stated that they seek mentor-ship guidance. 65% of these respondents seek mentor-ship for business modeling and fund management.

- 12% of respondents cite understanding and meeting regulatory standards as a challenge in their day to day business

- 881% of the respondents stated that the prices of c0-working spaces is too high which result in increased infrastructure costs

-

Policy Environment

- 50+ Schemes introduced by Govt in last 5 years to assist the growth of Startups & SMEs.

- Startup Grants and Schemes are accessible and their eligibility and other related details are easily available on the Ministry’s websites.

- Pradhan Mantri Jan Dhan Yojana and the related Jan Dhan, Aadhaar and Mobile number (JAM) trinity has the potential to link all Indians into one common financial, economic, and digital space. This brings India closer to the better financial inclusion.

- RBI set up an inter-regulatory working group to study the regulatory issues faced by fintechs, headed by Shri Sudarshan Sen.

- Many fintech companies are working in different ways to contribute towards achieving deeper financial inclusion in areas such as micro-finance, digital payments, credit scoring and remittances.

- 87% Of Respondents Suggested The Need Of A Regulatory Sandbox

- The need for flexible regulations or exceptions in ‘emerging’ areas like block-chain, alternative lending, database management and scoring models, outsourcing of core operations of Banks within the restricted experimental phase with adequate information security measures in place; was observed.

Recommendations by IFOR

IFOR considered the leading fintech hubs are benchmarks for development and understood its listed of growth. Based on the extensive research and considering the above mentioned findings in the Indian fintech landscape; IFOR recommends:

The creation of a Fintech Hub can help India take the LEAP into a world class ecosystem:

L – Lighter Regulatory Compliance

E – Enabling Environment

A – Augment Infrastructure

P – Partnership with global Hubs

Lighter Regulatory Compliance

IFOR suggests developing the following:

- Regulatory Sandbox: Regulatory Sandbox is a test environment and has proven results globally. It would be a common ground for Fintechs to test their products and business models along-with their impact on end consumers. Global Sandbox models provide relaxation, for a limited time period, in the regulations for the fintech startups.

- Regulatory Advisory Group: The Advisory Group will provide guidance to Fintechs on regulation and compliance in India and share their findings with the concerned regulators. The Group would consist of experts from each of the fintech domain along with Industry veterans such as investors and legal advisers.

- Fintech Association: It will be the single point entity for the fintech industry, similar to the Indian Banking Association (IBA) and the National Association of Software and Services Companies (NASSCOM). The entity can consolidate the efforts and help in creating a formal counsel for budding entrepreneurs.

- Creation of an Open Data or API Framework: IFOR recommends creation of relevant APIs (both informational and transactional) for delivering Government to Citizen (G2C), Government to Business (G2B), Government to Government (G2G) and Government to Employee (G2E) services in a timely and cost effective manner.

Enabling Environment

IFOR suggests setting up the following:

- Setting up a a Fintech Registry: The proposed Fintech registry would enable potential investors, policy makers, regulatory agencies and industry partners to study the Fintech landscape and identify opportunities for investment. The registry should also consist of the platform technology solutions like Big Data Analytics and AI, along-with Fintechs.

- Set up a dedicated PoC fund to boost PoC funding: Within the Start-up India Fund, a special fund for PoC funding in order to promote more experimentation within the financial services sector.

- Develop future human capital: A multi-disciplinary approach, if adopted by the universities, would help nurture the pool of human capital that is driven by research and specializes in Leadership.

Augment Infrastructure

IFOR suggests the creation of Innovation Labs to foster innovation in the Fintech. Some of the suggested Innovation Labs are as under:

1. MSME Innovation Lab

2. Financial Inclusion Lab

3. Smart City Innovation Lab

4. Farm-tech/Agri Innovations Lab

Partnership with Global Hubs

IFOR recommends developing ‘Fintech Bridges’ with leading fintech hubs of the world for transfer of knowledge. It will assist in innovation and conduct collective research towards regulatory issues. The bridge will help nurture future talent by providing greater exposure and share emerging trends.

Conclusion:

All of the above mentioned findings and recommendations, threw up light on the relevant details of the Indian Fintech Landscape- the present scenario and steps for a progressive future. The overall picture; all the stake holders; offer a positive outlook towards the Indian Fintech Landscape. The confidence in the Eco-system is highlighted by the fact that 77% of the respondents expect more than 100% revenue growth in the next 12 months, while 25% expect 200% + growth.

With the recommended steps, the fintech ecosystem is likely to blossom. IFOR states, ” Mumbai the Financial hub of the country and Bangalore the startup hub present themselves as natural choices with Mumbai having the edge housing all major consumers of financial technologies, a strong academic sector and the hub for all the financial services regulators”.

Source: Indias Fintech Landscape, a YES Bank Initiative.

- Posted on Oct 15, 2018

- |

- By Leena Bhagchandani

- |

- 0 Comments

Leave a Reply